After my article, “The Danger of leaders Not Listening“, I was asked why I thought many see the economy as struggling, despite signs of growth. I believe this sentiment stems largely from the significant changes brought about by COVID-19. When comparing pre-COVID prices to current ones, they are indisputably higher, reflecting an increased cost of living. The economic baseline from before COVID no longer applies.

Historical events like the post-WWII growth period show how economic baselines need reassessment after major disruptions.

Unfortunately, no one has clearly explained to the average American how COVID-19 affected the cost of living (and GDP). People blame the government for not controlling costs, but it’s challenging amid such upheavals. After events like COVID-19, a major realignment occurs, and the economy begins to grow again from this new baseline.

One major factor in the economy’s struggle is the shift to a more digital and remote lifestyle.

This transition was accelerated by COVID-19, forcing many businesses and industries to adapt quickly in order to survive. This resulted in job loss for some and increased competition for others, leading to financial instability and uncertainty.

Additionally, the pandemic highlighted existing inequalities within our society, particularly in terms of access to resources and opportunities. COVID-19’s economic impact hit marginalized communities harder, making recovery from the pandemic’s disruptions even more difficult.

Furthermore, there were concerns about inflation as a result of the massive amounts of government stimulus put into place during the pandemic. This led to fears of rising prices and a decrease in purchasing power for individuals and businesses.

To understand the economic struggles, we must also consider COVID-19’s psychological impact on consumer behavior.

Many people were more cautious with their spending, prioritizing essential items over non-essential purchases. This change in consumer behavior greatly affected businesses and their ability to thrive in that economic climate.

Overall, it is clear that COVID-19 had a significant impact on the economy and its recovery. Leaders must acknowledge the challenges and find sustainable solutions for both current struggles and long-term impacts. As we continue to navigate the pandemic’s impact, individuals should educate themselves on economic changes and adapt. Only then can we work towards a more stable and resilient economic future.

The effects of COVID-19 will be felt for years, so leaders should listen to concerns and address them proactively.

This includes supporting those most affected by the pandemic and implementing policies that promote economic growth and stability.

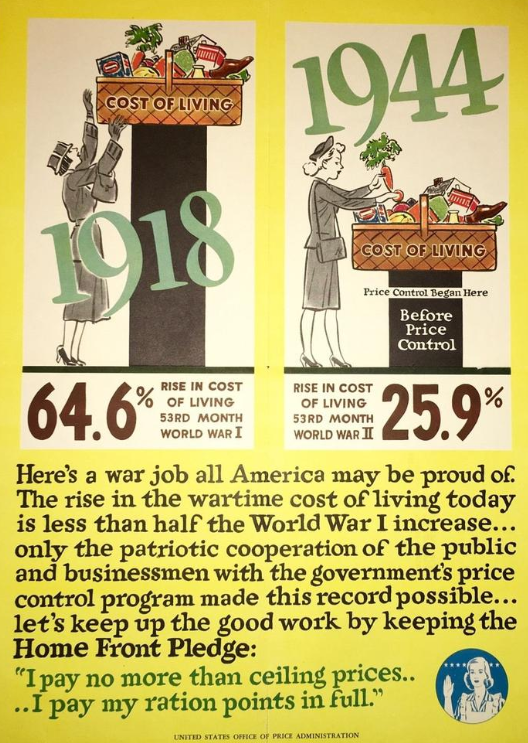

WWII as a Disruptive Event

The last major event to impact the economy like COVID (rapid GDP swings), with widespread business shutdowns and supply limitations, was World War II. Before WWII, the cost of living was lower due to economic stability and fewer disruptions. However, the war introduced significant shifts in production, supply and demand, and heightened government intervention, all of which influenced prices. After the war ended and production returned to normal, prices remained higher than before, resulting in a new economic baseline.

Like COVID-19, the aftermath of WWII required reassessing economic baselines for growth and stability. This teaches us to focus not only on short-term recovery but also on long-term solutions for a sustainable economy. Leaders then had to listen to individuals’ concerns, and it’s crucial for leaders today to do the same to guide us through uncertainty.

What Is Gross Domestic Product (GDP)?

Gross domestic product (GDP) represents the total monetary value or market worth of all finished goods and services produced within a country during a specific time period. Serving as a broad indicator of a nation’s overall economic output, GDP acts as a comprehensive measure of the country’s economic health.

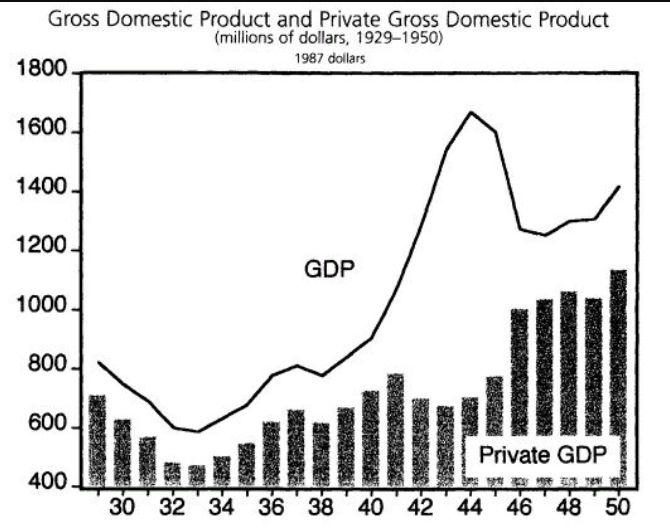

Before World War II, the U.S. GDP was stable, but it surged as the country ramped up production for a wartime economy, retooling factories and hiring workers. After the war, GDP experienced a significant decline as factories adapted to a peacetime economy, leading to reduced production and substantial layoffs.

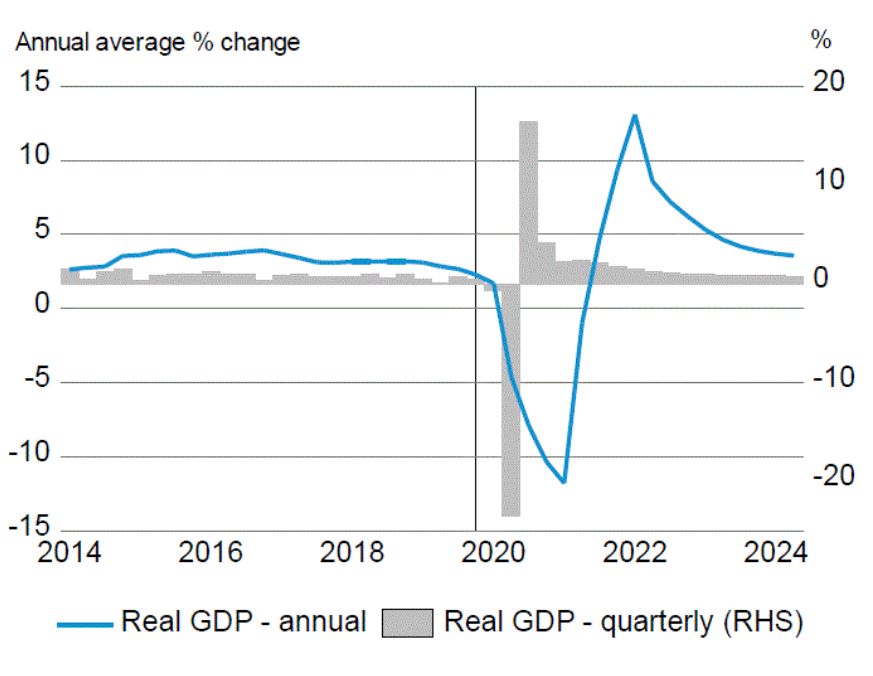

Before COVID, the U.S. GDP was stable following the recovery from the 2008 financial crisis. However, when the pandemic struck, GDP plummeted as production halted and businesses closed. As the pandemic receded, GDP soared with the resumption of business activities, restaurant openings, and more. This resurgence caused a notable increase in GDP, leading to a higher cost of living and rising prices.

The chart illustrates that from 2020 to 2024, there were fluctuations reflecting the adverse cost of living impacts faced by the average American.

Volatile GDP fluctuations challenge wage growth, making it hard to keep pace. Despite GDP surpassing pre-COVID levels, wage and price stabilization is only now emerging. As the economy continues to recover, workers continue to grapple with stagnant wages and increasing living costs.

In conclusion, both COVID-19 and World War II serve as prominent examples of major events that have significantly disrupted the economy. These disruptions not only create short-term challenges but also require a reassessment and adaptation to new economic baselines in order for long-term stability and growth to occur. Understanding the impacts of these events on GDP is crucial in navigating through these changes and creating sustainable solutions for the future. So, it is essential to constantly monitor GDP and make necessary adjustments in response to major disruptions, ensuring a stronger and more resilient economy for all.

Click here for a post on the pandemics influence on technology.